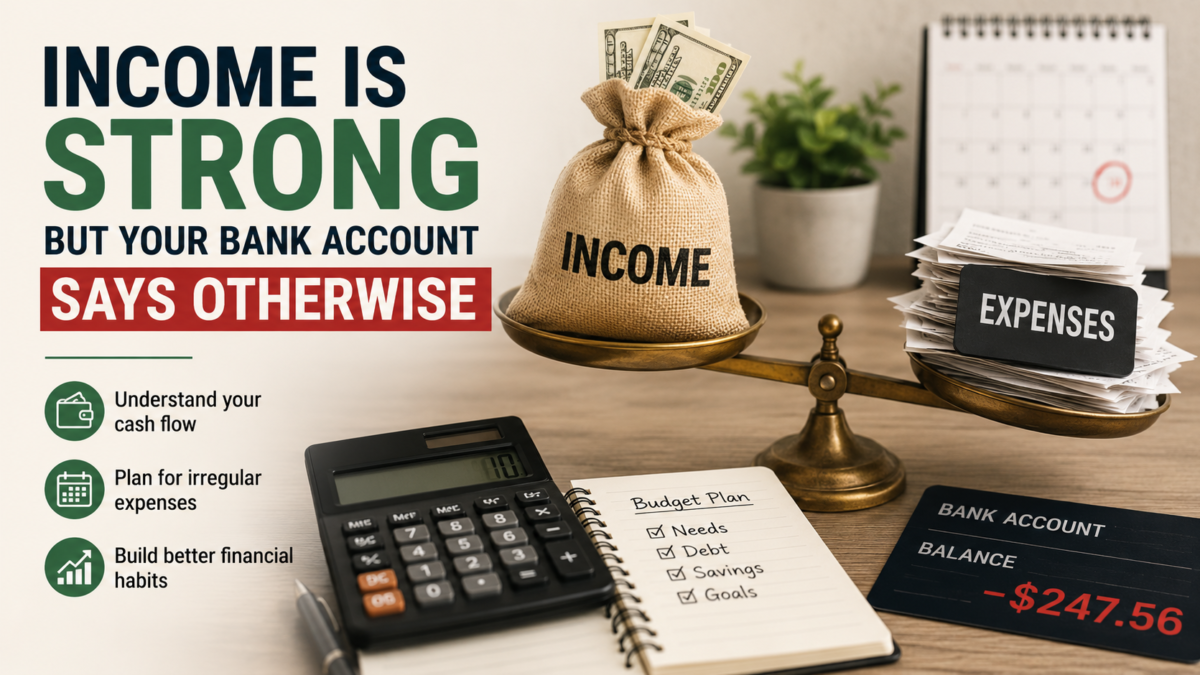

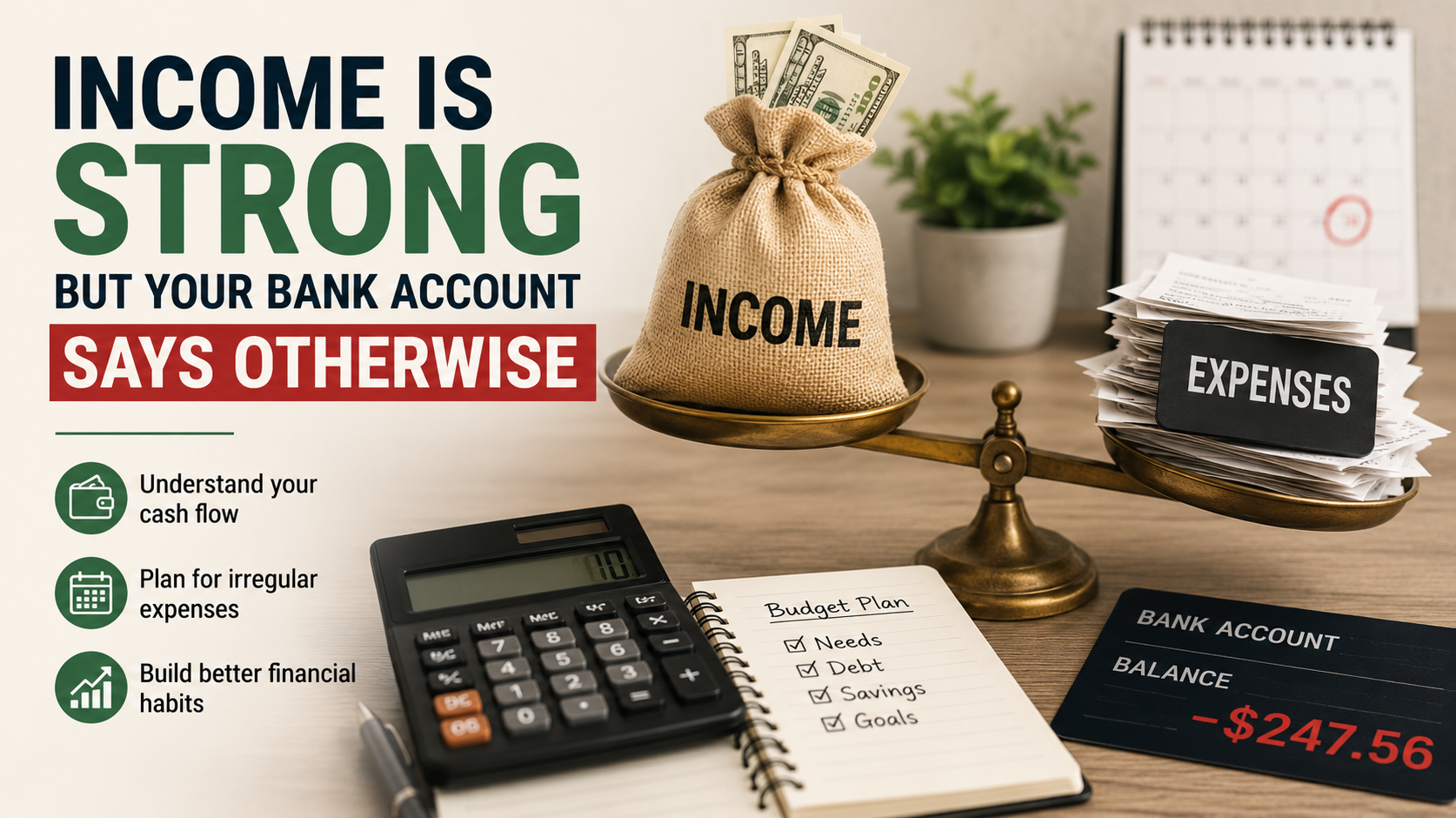

A strong income should feel reassuring, yet many people find themselves in a strange position. The paycheck looks good on paper, but the bank balance keeps telling a different story. That disconnect can be frustrating because it creates confusion. If the income is solid, why does cash still feel tight?

Sometimes the answer has little to do with how much you earn and a lot to do with how money flows. That is why someone may start exploring a California debt relief program and then realize the bigger issue is cash flow, not simply income level. Money may be coming in, but it is leaving in ways that are less visible, less planned, or more delayed than expected.

This is where practical tools from MyMoney.gov and Consumer.gov’s budgeting guidance become useful. They help separate the idea of earning well from the reality of managing cash well. Those are not always the same skill, and treating them as identical can hide the real problem.

Income and cash are not the same thing

One of the biggest misunderstandings in personal finance is assuming that good income automatically creates financial ease. It does not. Income tells you how much is coming in over time. Cash tells you what is actually available right now after obligations, timing issues, and existing commitments are accounted for.

A person can earn well and still feel squeezed if bills are high, debts are heavy, expenses are irregular, or spending is loosely managed. In some cases, income arrives in chunks that do not match monthly obligations well. In others, the problem is that a large percentage of earnings is already spoken for before the money lands.

This is why a healthy salary can still coexist with a stressed checking account.

Lifestyle growth can quietly absorb progress

A common reason strong income fails to create strong cash position is lifestyle growth. As earnings rise, spending often rises too. The changes may not feel dramatic. A nicer apartment, more dining out, higher subscriptions, more travel, better clothes, upgraded routines, or added convenience costs can slowly expand to match the new income.

The tricky part is that none of these decisions may seem reckless individually. Together, though, they can absorb nearly all progress. You end up earning more without feeling more stable. In some cases, you may feel even more pressure because fixed expenses have increased.

This can create the illusion that income is somehow disappearing, when really it is being assigned almost instantly to a more expensive version of daily life.

Irregular expenses create hidden leaks

Another reason income can feel strong while cash feels weak is that many expenses are not truly monthly. Insurance renewals, car repairs, travel, gifts, school costs, health costs, and home maintenance all arrive on uneven schedules. If you are not planning for those costs in advance, the bank account may always seem to dip unexpectedly.

That can make you feel like you should be doing better than you are. In reality, the missing piece may simply be preparation. Irregular expenses often make income feel less effective because they keep interrupting the normal monthly rhythm.

When those costs are accounted for, the picture usually becomes clearer.

High income can hide weak systems

A strong income can mask poor structure for a surprisingly long time. If enough money keeps coming in, you may not feel immediate pressure to build categories, track spending, or review cash flow carefully. But eventually the lack of system starts showing up in the bank balance.

This is why some people with modest incomes feel more in control than people who earn much more. It is not only about the size of the paycheck. It is about whether money has a system. Without one, cash tends to drift toward convenience, urgency, and short term wants.

A high income without a clear structure can still produce a low sense of stability.

The issue may be timing, not weakness

Sometimes the problem is not overspending but timing. Bills may hit before key deposits arrive. Variable income may create uneven months. Large expenses may cluster together. If the timing of inflows and outflows is misaligned, the bank account can look weak even when annual income is healthy.

This matters because it changes the solution. The answer may be a buffer account, a better bill schedule, or clearer paycheck allocation rather than a dramatic lifestyle overhaul. Once timing improves, the same income can start feeling much more supportive.

Cash flow clarity changes everything

When income is strong but the bank account says otherwise, the most useful response is not shame. It is clarity. Look at what is fixed, what is variable, what is irregular, what is debt related, and what is simply drifting out without enough attention. Once those patterns are visible, the mystery starts to disappear.

That matters because confusion creates stress. Clarity creates options. You may find that the issue is not that you are failing. It is that your money needs better direction, better timing, or better boundaries.

A strong income is valuable. But income alone does not create peace. Structure does. When the flow becomes clearer, the bank account starts telling a different story.

{kind=link}