Table of Contents

Introduction

The financial landscape in 2025 looks dramatically different from just five years ago. The rise of neobanks—digital-only banks with no physical branches—has disrupted the market, offering slick apps, faster service, and innovative features. At the same time, traditional banks are modernizing rapidly, leveraging technology, vast resources, and customer trust built over decades.

So, in the clash between neobanks and traditional banks, who’s winning? Let’s explore.

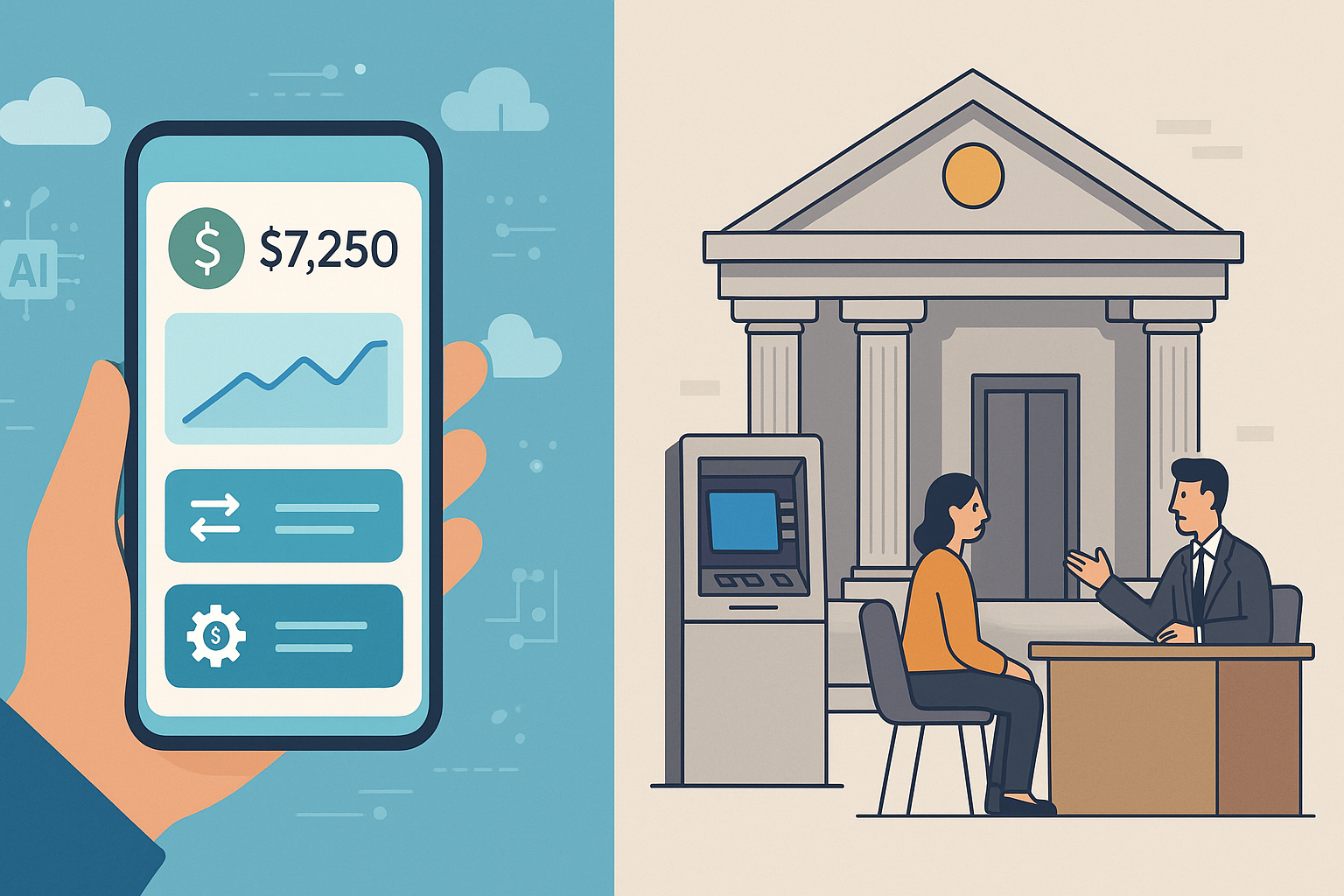

What Are Neobanks?

Neobanks are digital-first financial institutions that operate entirely online. They have no brick-and-mortar branches and typically focus on offering:

- Mobile-first banking apps

- Low or no fees

- Fast onboarding

- Real-time insights into spending and saving

- Seamless international transactions

Examples of neobanks include Revolut, N26, Monzo, Jupiter, and Fi Money in India.

What Are Traditional Banks?

Traditional banks have been the backbone of global finance for centuries. These institutions offer:

- Full-service banking — savings, loans, credit cards, mortgages, investments

- Large branch and ATM networks

- Human support in-branch and via call centers

- Strong regulatory standing and reputation

Big names include State Bank of India (SBI), HDFC Bank, ICICI Bank, Chase, and HSBC.

See Also: Top FinTech Stocks to Watch in 2025: From Digital Banks to Blockchain Innovators

Why Neobanks Are Gaining Ground in 2025

- Customer-Centric Design: Neobanks have reimagined banking around user experience. Their apps are intuitive, fast, and transparent, catering to mobile-first generations.

- Low Fees and Better Rates: Without physical branches to maintain, neobanks offer lower overhead costs. This lets them provide better interest rates and fewer fees.

- Personalized Features: AI-driven insights, budgeting tools, and real-time notifications help users manage finances smarter.

- Faster Innovation: Neobanks can roll out new features quickly thanks to agile technology stacks and lean structures.

- Appeal to Underbanked: In regions where traditional banking access is limited, neobanks fill a critical gap.

How Traditional Banks Are Fighting Back

- Digital Transformation: By 2025, most traditional banks have significantly modernized their digital offerings. Top-tier apps, instant payments, and AI-powered chat support are standard.

- Omni-channel Strength: Traditional banks provide the best of both worlds: digital convenience and human support at branches when needed.

- Regulatory Edge & Trust: Long-standing institutions benefit from deep regulatory relationships, large compliance teams, and consumer trust built over generations.

- Partnerships & Acquisitions: Many traditional banks have partnered with or acquired FinTech startups to accelerate innovation.

Neo banks vs Traditional Banks: Key Comparisons

| Feature | Neobanks | Traditional Banks |

|---|---|---|

| Branches | Digital-only | Nationwide/international branch networks |

| Fees | Often low/no fees | Typically higher fees |

| Speed of Service | Fast onboarding, instant payments | Slower processes in some cases |

| Product Range | Limited at times (e.g. no mortgages) | Comprehensive (loans, investments, insurance) |

| Customer Support | Mostly chat-based | Phone, in-branch, and online |

| Trust Factor | New entrants building trust | Established trust over decades |

Who’s Winning in 2025?

The truth? Both are thriving in different ways.

- Neobanks are winning younger, tech-savvy customers who value speed, transparency, and innovative tools.

- Traditional banks are holding onto high-net-worth individuals and customers who want a full range of services and the option for in-person help.

What’s clear is that the banking sector is no longer a zero-sum game. The future is hybrid — customers want digital-first convenience with the safety net of trusted institutions.

What’s Next?

Expect to see:

- More hybrid models: Traditional banks launching neobank-like apps and neobanks offering more traditional products.

- Deeper AI integration: For fraud detection, credit scoring, and personalized financial advice.

- Regulatory evolution: As neobanks mature, regulators will bring stricter oversight, leveling the playing field.

- New partnerships: Between banks, FinTech, and Big Tech (think Google Pay, Apple Pay, WhatsApp Payments).

Final Thoughts

In 2025, the question isn’t neobank or traditional bank — it’s how both can coexist and collaborate to deliver better banking experiences. The winners? Customers, who benefit from more choices, better tech, and stronger service.

👉 Explore more on FinTech innovation at iTMunch

{kind=link}